How Credit Scores Work in Canada: Score Ranges, Tips and FAQ

By Canooq Editorial

June 3, 2026

A beginner-friendly guide to Canadian credit scores: what they are, how they work, what helps, what hurts, good score ranges, and what to do next.

QUICK START

Credit is a track record, not a personality score.

A Canadian credit score summarizes how your credit file looks to a bureau or lender model.

- Pay on time.

- Use a small share of your available credit.

- Opening many cards can hurt if it creates hard checks, new accounts, fees, or balances.

Buying later?

Use this as a planning guide, then confirm details with the linked source before you act.

What's on this page

Canadian credit scores are based on credit-report information. Pay on time, keep balances low, and apply for credit deliberately.

Credit basics

Credit scores are a shortcut lenders use to read your borrowing history.

In Canada, your score is built from your credit report activity. It can help with credit cards, rentals, car loans, mortgages, and some phone plans, but it is only one part of an approval.

- The two big Canadian credit bureaus are Equifax and TransUnion.

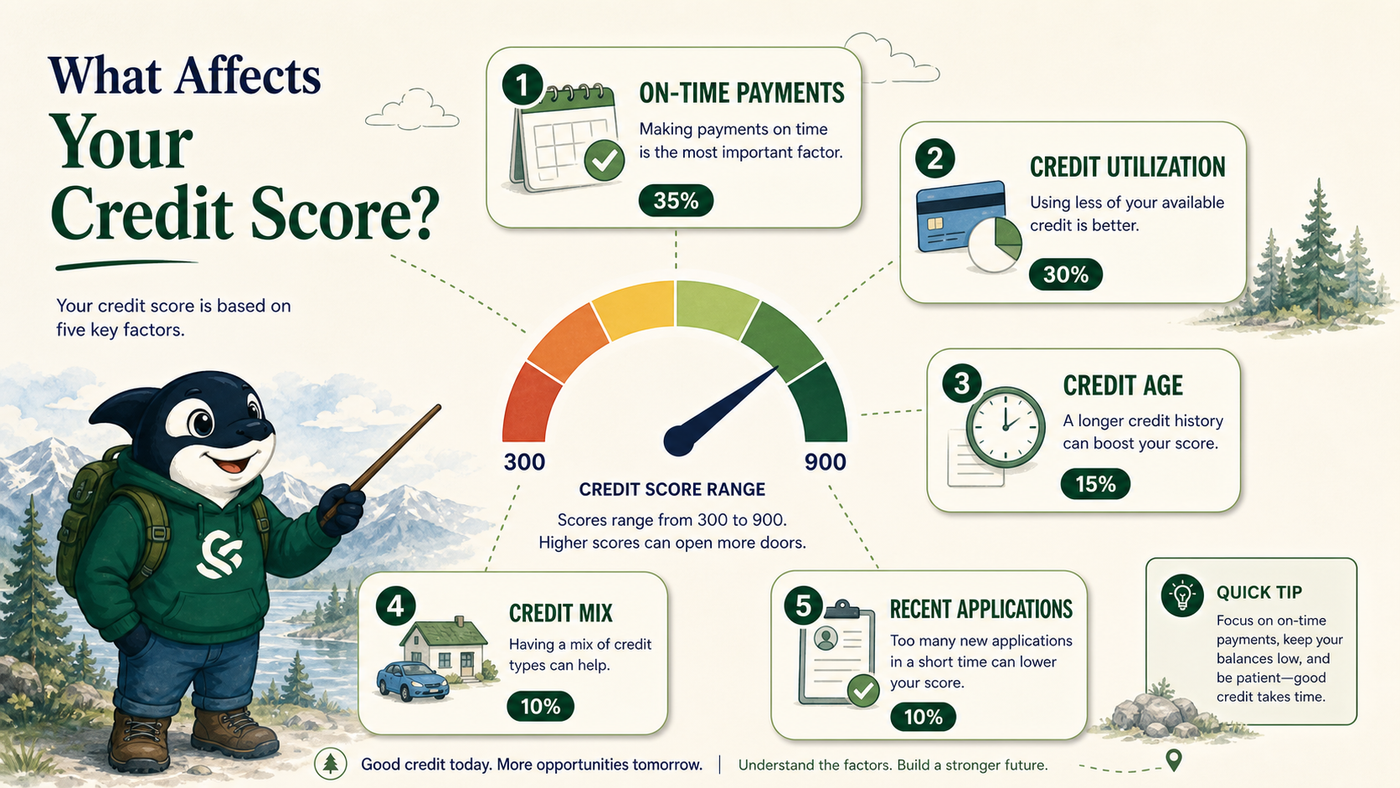

- Payment history and credit utilization usually matter the most.

- Opening cards is not automatically bad; opening many quickly can create hard inquiries and lower account age.

- Good credit habits are simple: pay on time, keep balances low, and check reports for errors.

Estimate the habits that move a score

Use the guide below to decide what to check next.

What is a credit score?

A credit score is a three-digit estimate of credit risk. It tries to answer a simple lender question: based on this person's past credit behaviour, how likely are they to repay borrowed money on time?

Your score is based on information in your credit report, not your personality, savings account balance, immigration story, job title, or how responsible you feel. The report usually includes credit cards, lines of credit, loans, mortgages, payment history, credit limits, balances, collections, public records, and recent credit checks.

How credit scores work in Canada

- Credit bureaus collect report data. Equifax and TransUnion receive information from lenders and other reporting organizations. Your score can differ between bureaus because each may have different data and scoring models.

- Lenders choose how to use the score. A bank, card issuer, car lender, landlord, telecom provider, or mortgage lender may look at the score, the report details, income, debt, employment, assets, identity, and their own rules.

- Scores update as reports update. A credit card balance, payment, new account, or hard inquiry may not show instantly. Many lenders report monthly.

- There is no single universal score. You may see one score in an app and a lender may use another version. Focus on the underlying habits more than one exact number.

What a credit score is helpful for

- Credit card approvals, credit limits, and promotional offers.

- Car loans, personal loans, and lines of credit.

- Mortgage preapproval and rate discussions, although income, down payment, property, and debt ratios still matter heavily.

- Rental applications when a landlord or property manager checks credit.

- Some phone plans, utility accounts, and buy-now-pay-later or financing offers.

What helps your score

- Pay every bill on time. Payment history is one of the biggest signals. Automate at least the minimum payment if you can.

- Keep utilization low. Utilization is the balance compared with the credit limit. A $900 balance on a $1,000 card looks tighter than a $900 balance across $10,000 of total limits.

- Let good accounts age. Older accounts can help because they show longer history. Closing an old no-fee card can reduce average age and available credit.

- Use a mix carefully. A credit card, line of credit, instalment loan, or mortgage can all show different types of repayment, but do not borrow just to create a mix.

- Check reports for errors. Wrong addresses, unfamiliar accounts, duplicate collections, or incorrect late payments should be disputed quickly.

What hurts your score

- Late or missed payments. Even one late payment can hurt, especially if it is reported as 30, 60, or 90 days late.

- Maxed-out cards. High utilization can make you look stretched even if you always pay eventually.

- Collections, defaults, consumer proposals, or bankruptcies. These can stay visible for years and matter a lot to lenders.

- Many hard inquiries in a short period. Several applications close together can signal risk. Rate shopping for some products may be treated differently, but random applications can still add noise.

- Very new credit history. A thin file is not bad behaviour, but lenders have less proof to evaluate. Newcomers and young adults often need time to build history.

Is it bad to open many credit cards?

Opening credit cards is not automatically bad. A new card can add useful available credit, rewards, insurance, a welcome bonus, or a no-fee backup card. The risk is opening too many in a short window, carrying balances, missing payments, or creating spending pressure.

- Good reason to open one: you want a useful card, can meet the conditions, will pay it in full, and do not need a major loan immediately.

- Bad pattern: you apply for several cards quickly, chase bonuses without tracking due dates, and let balances climb.

- Mortgage timing: if you are close to a mortgage application, avoid unnecessary new credit unless your broker or lender says it is fine.

Does credit score matter a lot?

It matters, but not equally everywhere. For a basic credit card, the score can be central. For a mortgage, the score matters, but income, employment, down payment, debt ratios, property value, and documentation can matter just as much or more. For renting, some landlords care deeply and others care more about income, references, and timing.

Good credit practices

- Turn on automatic minimum payments, then manually pay the full statement balance when possible.

- Keep card balances comfortably below limits before statement dates if you are trying to improve utilization.

- Do not ignore a disputed or unfamiliar account. Pull both bureau reports and fix errors.

- Keep a no-fee older card open if it is not causing problems.

- Use calendar reminders for annual fees, promotional periods, and balance transfers.

- Do not co-sign casually. A missed payment on co-signed debt can become your credit problem.

What is a good credit score range?

Ranges vary by bureau, lender, and scoring model, but a common education-friendly way to think about it is: below 560 needs work, 560 to 659 is fair, 660 to 724 is good, 725 to 759 is very good, and 760+ is excellent. A score around the mid-600s can already be usable for many products, while a very strong score can help with smoother approvals and better pricing.

FAQ

Should I pay my credit card before the statement date?

If utilization is high, paying before the statement can help because the reported balance may be lower. The most important rule is still to pay by the due date.

Will checking my own score hurt it?

No. Checking your own credit through a consumer app, bank tool, or credit bureau is normally a soft check and does not hurt your score.

How long does it take to build credit?

You can start building history within months, but a strong profile usually takes repeated on-time payments over time. Thin files become stronger when they show consistency.

Should I close a credit card I do not use?

If it has no fee and no temptation risk, keeping it open can help account age and available credit. If it has a fee, security concern, or spending risk, closing can still be sensible.

What should I do after a missed payment?

Pay it as soon as possible, contact the lender, turn on automatic minimum payments, and watch both credit reports. If the report is wrong, dispute it with the bureau and the lender.

Do newcomers start with a bad score?

Usually they start with little Canadian history, not a bad history. A secured card, newcomer banking package, phone plan, or small starter card can help create report activity.

Related articles:

Page details

Author: Canooq Editorial

Updated: June 3, 2026

Cite this page: Canooq.ca, How Credit Scores Work in Canada: Score Ranges, Tips and FAQ, https://canooq.ca/blog/how-credit-scores-work-canada

Canooq content is educational and may include affiliate or referral links. It is not financial, tax, legal, immigration, employment, mortgage, real estate, or healthcare advice. Verify official sources and provider terms before acting.