TFSA vs Non-Registered Account in Canada: Which Should You Use First?

June 16, 2026

A beginner-friendly comparison of TFSAs and non-registered investment accounts in Canada, including contribution room, withdrawals, taxes, capital gains, interest, dividends and when to use each.

TFSA VS TAXABLE

Check TFSA room before taxable investing.

A TFSA shelters growth from Canadian tax. A non-registered account gives unlimited space but creates tax reporting.

- TFSA growth and eligible withdrawals are generally tax-free in Canada.

- Non-registered accounts can trigger tax on interest, dividends, foreign income and realized capital gains.

- Use taxable investing when registered room is full, reserved or not appropriate for the goal.

Check your room

Use the linked guides and tools to go deeper when a step applies to you.

What's on this page

Use TFSA room first for many goals because growth and eligible withdrawals are generally tax-free in Canada. Use non-registered investing when room is full, reserved or not suited to the goal.

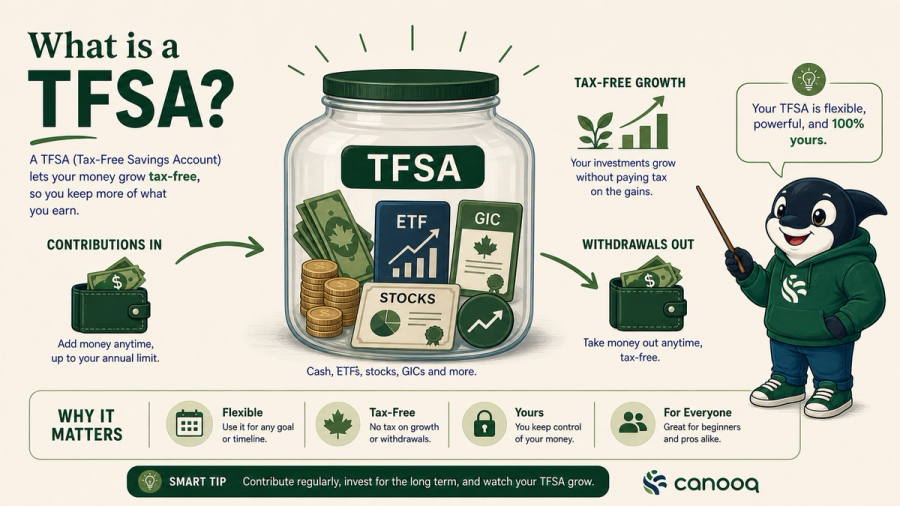

A TFSA and a non-registered account can hold many of the same investments. You can hold cash, GICs, ETFs, mutual funds and stocks in either type of account if the provider supports them. The difference is the tax wrapper. The TFSA gives you tax-free growth in Canada, but only up to your contribution room. The non-registered account gives you more space, but it creates tax reporting.

For many beginners, the TFSA is the first account to check. It is flexible, clean and powerful. You can use it for long-term investing, a future home, retirement, a sabbatical, emergency overflow or a major purchase. If the money grows inside the TFSA and you follow the rules, the growth does not get taxed in Canada when you withdraw it.

Why the TFSA is so useful

The TFSA has three advantages that matter for beginners. First, eligible income and gains inside the account are generally tax-free in Canada. Second, eligible withdrawals do not count as taxable income. Third, withdrawals usually come back as new contribution room on January 1 of the following year.

That flexibility makes the TFSA easier to use than an RRSP for many early-career goals. If you are still learning the basics, start with TFSA Explained Canada and check your estimated room with the TFSA contribution room calculator.

Contribution room is the catch. If you contribute too much, CRA can charge penalties. Your CRA account can also lag behind recent deposits and withdrawals, so you should track your own contributions. This matters even more if you use several banks or brokerages.

For the room rules, check CRA guidance and track your own contributions because CRA account room can lag behind recent deposits and withdrawals.

WealthsimpleWealthsimple offers a $25 referral bonus for the referee. Wealthsimple is a Canadian investing and money management platform.InvestingCashTFSARRSPFHSA

WealthsimpleWealthsimple offers a $25 referral bonus for the referee. Wealthsimple is a Canadian investing and money management platform.InvestingCashTFSARRSPFHSAHow a non-registered account is taxed

A non-registered account is a regular taxable investment account. It has no TFSA-style contribution limit. You can add more money, hold more investments and withdraw when you want. The tradeoff is tax reporting. You may receive tax slips, and you may need to track adjusted cost base, realized gains, losses and foreign income.

Non-registered tax basics

This is the plain-language version for Canadian tax residents.

| Investment income | What usually happens | Why it matters |

|---|---|---|

| Interest and GIC income | Taxed as regular income | Cash and GICs can be tax-heavy outside registered accounts. |

| Canadian dividends | Reported with gross-up and dividend tax credit rules | The tax treatment differs from interest. |

| Capital gains | Tax usually applies when you sell for more than your adjusted cost base | You need clean records of buys, sells and reinvested distributions. |

| Foreign income | Usually taxable in Canada and may involve withholding tax | Currency conversion and slips can add complexity. |

Taxable accounts can still be excellent. Many Canadians use non-registered accounts once TFSA, RRSP and FHSA room is used or reserved. A taxable account gives extra investing space and flexibility. It just asks you to keep records and understand the tax slips.

When TFSA should usually come first

The TFSA deserves first look when you still have room and your goal needs flexibility. It works well for long-term ETF investing, cash you want to shelter from tax, a future down payment if an FHSA does not fit, a career break fund, or retirement money you may want before traditional retirement age.

- You have unused room. Unused TFSA room is valuable because future growth can stay tax-free in Canada.

- You want simple withdrawals. Eligible withdrawals do not create taxable income and usually restore room next year.

- You dislike tax paperwork. The TFSA avoids annual taxable reporting for the investments inside it.

- Your income may rise later. A TFSA can make more sense than using RRSP deductions in a low-income year.

When non-registered investing makes sense

A non-registered account starts to make sense when your registered account room is full, when you are investing more than registered limits allow, or when a taxable account fits the planning better. It can also make sense if you want no registered withdrawal rules, if you are saving for flexible goals after TFSA room is used, or if you have a large amount to invest.

The account also fits investors who are comfortable with record keeping. You need to know what you bought, what you sold, what income you received and what your adjusted cost base is. If that sounds annoying, that is another reason to use TFSA room first while you have it.

Common account choices

TFSA or non-registered first?

Use the account that fits the goal and tax situation.

| Situation | First account to check | Why |

|---|---|---|

| Beginner with TFSA room | TFSA | Tax-free growth and fewer tax slips |

| Long-term ETF investing with unused room | TFSA | Shelters compounding |

| TFSA room already used | Non-registered | No contribution limit |

| Emergency fund overflow | TFSA or high-interest cash | Depends whether you need TFSA room for growth investments |

| First-home buyer who qualifies | FHSA before TFSA for home money | FHSA can combine a deduction and tax-free qualifying withdrawal |

| High-income investor saving a lot | Non-registered after registered room | Extra space for money above account limits |

The broader registered-account comparison is TFSA vs RRSP vs FHSA. If you want a simple investing style, read Couch Potato Investing in Canada.

Use these next

Check room first, then choose the account.

Related articles:

Page details

Author: Canooq Editorial

Updated: June 16, 2026

Last reviewed: June 16, 2026

Cite this page: Canooq.ca, TFSA vs Non-Registered Account in Canada: Which Should You Use First?, https://canooq.ca/blog/tfsa-vs-non-registered-account-canada

Canooq content is educational and may include affiliate or referral links. It is not financial, tax, legal, immigration, employment, mortgage, real estate, or healthcare advice. Verify official sources and provider terms before acting.