TFSA Explained: How Tax-Free Savings Accounts Work in Canada

By Canooq Editorial

June 1, 2026

A beginner-friendly TFSA guide covering contribution room, withdrawals, investing, taxes, newcomers, and common mistakes.

QUICK START

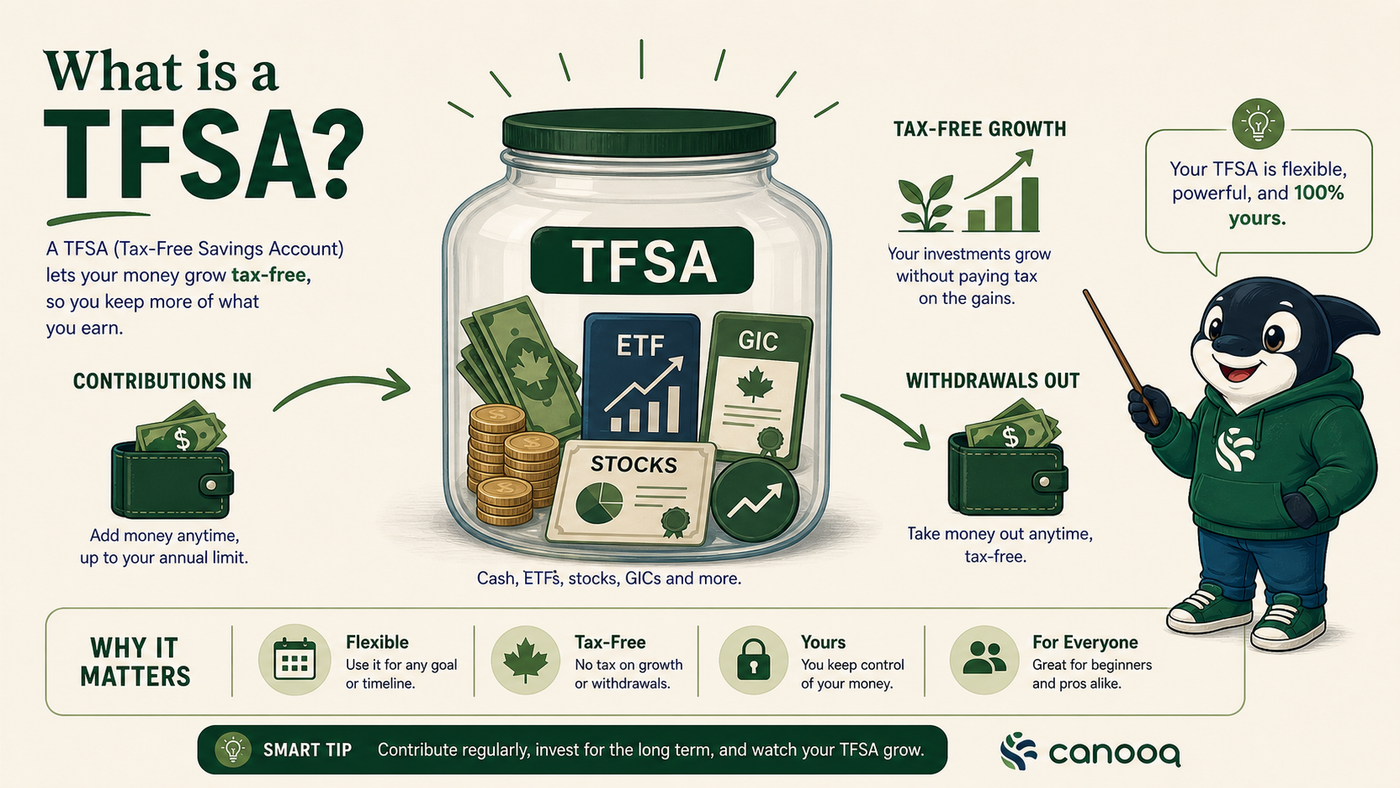

A TFSA is a tax shelter, not only a savings account.

Cash can sit inside a TFSA, but so can many investments. Match the holding to the goal.

- TFSA contributions are not tax deductible.

- Eligible growth and withdrawals are generally tax free.

- Withdrawals come back as contribution room on January 1 of the following year.

Estimate your room

Use this article as a starting point, then check the linked official sources before acting.

What's on this page

A TFSA is a registered account where eligible growth and withdrawals are generally tax free. The key is contribution room, not the word savings.

What a TFSA does

TFSA stands for Tax-Free Savings Account. The name is a little misleading because the important part is not that it is a savings account. It is a registered account that can hold eligible cash or investments while sheltering eligible income, gains, and withdrawals from Canadian tax.

A TFSA does not create a tax deduction when you contribute. You put in after-tax money. The reward is that interest, dividends, and capital gains earned inside the account are generally not taxed, and eligible withdrawals do not count as taxable income.

Who can open and contribute

- You generally need to be 18 or older, have a valid SIN, and be a Canadian resident for tax purposes to earn TFSA room.

- Newcomers should not assume they have room for years before becoming Canadian tax residents.

- Non-residents can face special tax consequences for contributions, so confirm the rules before depositing if your residency status is unclear.

Contribution limits, deadlines, and penalties

The 2026 TFSA dollar limit is $7,000. Unused room carries forward, and withdrawals made in one year are generally added back on January 1 of the following year. There is no annual contribution deadline like RRSP season, but the calendar year matters because room resets on January 1.

The common penalty problem is overcontribution. If you contribute more than your available room, the CRA can charge tax of 1% per month on the excess amount until it is fixed or new room becomes available.

The contribution-room mistake

Your room depends on annual limits, age, Canadian tax residency, unused room, contributions, withdrawals, transfers, and corrections. CRA records are the safest source, especially if you are new to Canada, have withdrawn and recontributed, or have moved in and out of tax residency.

Estimate TFSA contribution room

Use Canooq's TFSA calculator as a planning estimate, then confirm your official room in your CRA account.

Open calculatorWhen to use a TFSA

A TFSA can fit several goals because withdrawals are flexible. It can be useful for an emergency fund, a medium-term savings goal, long-term investing, or retirement money that you may want to access without taxable withdrawals later. The shorter the timeline, the safer the holdings usually need to be.

What to hold inside a TFSA

- Emergency savings can use cash or high-interest savings if access matters.

- Short-term goals may fit cash or GICs because market risk can be awkward.

- Long-term goals may use diversified investments if you can handle market swings.

- Avoid speculative investments if losing the room would hurt. Investment losses inside a TFSA do not create new contribution room.

Advantages and disadvantages

- Advantages: tax-free eligible growth, tax-free eligible withdrawals, flexible access, and room restored the next calendar year after withdrawals.

- Disadvantages: no tax deduction, strict room tracking, penalties for excess contributions, and investment risk if you hold volatile assets.

TFSA vs RRSP vs FHSA

Use the TFSA when flexibility matters or when your current tax rate is low enough that an RRSP deduction is less valuable. Compare an RRSP when retirement tax planning and deductions matter. Compare an FHSA first if you qualify and are actively saving for a first home.

Compare the TFSA with RRSPs and FHSAs before deciding where each savings dollar belongs.

Where Wealthsimple fits for a TFSA

Wealthsimple can be a practical TFSA place if you want an app-first setup for cash or investing and you understand your contribution room. It is especially useful when you want simple account opening, low-friction recurring deposits, and beginner-friendly investing options. The account choice still comes first: use cash-like holdings for short-term money and diversified investments only for money that can handle market swings.

WealthsimpleWealthsimple offers a $25 referral bonus for the referee. Wealthsimple is a Canadian investing and money management platform.InvestingCashTFSARRSPFHSA

WealthsimpleWealthsimple offers a $25 referral bonus for the referee. Wealthsimple is a Canadian investing and money management platform.InvestingCashTFSARRSPFHSARelated articles:

Page details

Author: Canooq Editorial

Updated: June 3, 2026

Cite this page: Canooq.ca, TFSA Explained: How Tax-Free Savings Accounts Work in Canada, https://canooq.ca/blog/tfsa-explained-canada

Canooq content is educational and may include affiliate or referral links. It is not financial, tax, legal, immigration, employment, mortgage, real estate, or healthcare advice. Verify official sources and provider terms before acting.