FHSA Explained: Canada's First Home Savings Account for Beginners

By Canooq Editorial

June 1, 2026

Learn how FHSAs work in Canada, including eligibility, annual and lifetime limits, tax deductions, qualifying withdrawals, and TFSA or RRSP comparisons.

QUICK START

The FHSA is powerful if you qualify.

It can give a deduction on the way in and tax-free qualifying withdrawals for a first home.

- The annual contribution limit is $8,000, with a $40,000 lifetime limit.

- Eligibility and first-time home buyer rules matter before you open one.

- If you do not buy, transfer options and timelines become important.

Planning a first home?

Use this article as a starting point, then check the linked official sources before acting.

What's on this page

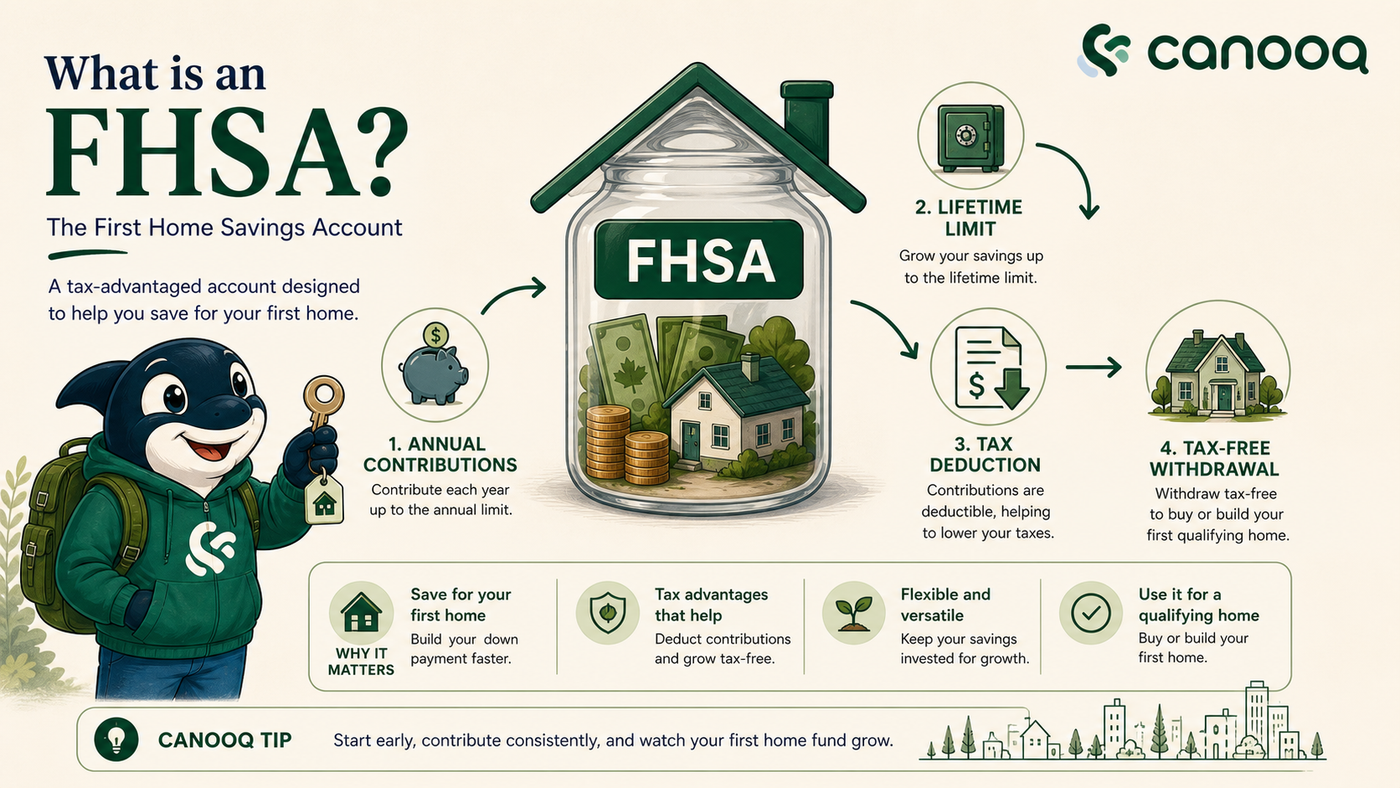

An FHSA combines RRSP-style deductions with tax-free qualifying withdrawals for eligible first-time home buyers. Eligibility matters before deposits.

What an FHSA does

FHSA stands for First Home Savings Account. It is a registered account for eligible first-time home buyers. Contributions can be deductible like an RRSP, and qualifying withdrawals for a first home can be tax free like a TFSA.

The FHSA is powerful because it can combine two benefits in one account. The catch is that the money has a specific purpose. If you do not use it for a qualifying home or transfer it properly, withdrawals may become taxable.

The rules to check before opening

- You generally must be a Canadian resident, at least 18, and a first-time home buyer under the FHSA opening rules.

- You need a valid SIN and an issuer that offers FHSAs.

- If you have recently lived in a home you owned or jointly owned, check the first-time home buyer test carefully before opening.

Contribution limits, deadlines, and penalties

The FHSA contribution limit is $8,000 per year and $40,000 over your lifetime. Unused FHSA participation room can carry forward, but generally only up to $8,000. Contribution room starts after you open your first FHSA.

FHSA contributions made in a calendar year are normally claimed for that year. If you contribute or transfer more than your FHSA participation room, the CRA can charge 1% per month on the highest excess amount in the month until the excess is fixed.

Qualifying withdrawals

A qualifying FHSA withdrawal can be tax free if you meet all required conditions. The home must be a qualifying home in Canada, you need a written agreement to buy or build, you generally cannot have acquired the home more than 30 days before the withdrawal, and you must intend to occupy it as your principal residence within one year after buying or building it.

If a withdrawal is not qualifying and is not another permitted withdrawal or transfer, it is generally taxable. That is why the FHSA should be tied to a real home-buying plan, not opened only because the tax treatment sounds attractive.

What to put inside an FHSA

- If you expect to buy soon, cash or GIC-style holdings may fit better than volatile investments.

- If the home goal is several years away, a conservative diversified portfolio may be reasonable, but market drops can still arrive at the wrong time.

- Do not invest FHSA money like long-term retirement money if you may need it for a down payment soon.

Advantages and disadvantages

- Advantages: deductible contributions, tax-free qualifying withdrawals, tax-sheltered eligible growth, and a clear first-home purpose.

- Disadvantages: strict eligibility, limited annual and lifetime room, taxable non-qualifying withdrawals, and timelines if you do buy or stop qualifying.

FHSA vs TFSA vs RRSP

If you qualify and are actively saving for a first home, the FHSA often deserves attention before using TFSA or RRSP room for the same down payment goal. The TFSA is more flexible if plans may change. The RRSP is mainly for retirement tax planning, though the Home Buyers' Plan can matter for some buyers.

For the full housing decision, read Should You Buy a Home in Canada?.

Where Wealthsimple fits for an FHSA

Wealthsimple can be a useful FHSA provider if you want a simple digital place to open the account, contribute, and choose cash or investing options. It is best when you already understand the first-home rules and want a low-friction way to keep the account separate from everyday spending. If your closing date, residency, co-buyer situation, or transfer plan is complicated, verify the rules before withdrawing.

WealthsimpleWealthsimple offers a $25 referral bonus for the referee. Wealthsimple is a Canadian investing and money management platform.InvestingCashTFSARRSPFHSA

WealthsimpleWealthsimple offers a $25 referral bonus for the referee. Wealthsimple is a Canadian investing and money management platform.InvestingCashTFSARRSPFHSARelated articles:

Page details

Author: Canooq Editorial

Updated: June 3, 2026

Cite this page: Canooq.ca, FHSA Explained: Canada's First Home Savings Account for Beginners, https://canooq.ca/blog/fhsa-explained-canada

Canooq content is educational and may include affiliate or referral links. It is not financial, tax, legal, immigration, employment, mortgage, real estate, or healthcare advice. Verify official sources and provider terms before acting.