8 Canadian Personal Finance Misconceptions That Can Lead You Astray

By Canooq Editorial

June 1, 2026

Renting, TFSAs, tax brackets, mortgage prepayments, debt, RRSPs, and market timing are full of half-true rules. This beginner-friendly guide explains eight common Canadian personal finance misconceptions.

TOP SUMMARY

Eight rules worth questioning

Most money myths begin with a useful idea that has been stretched into a rule. The details matter, and the better answer often depends on your goals, rates, and timeline.

- A TFSA can hold investments, and a raise does not make every dollar taxable at a higher rate.

- Renting, mortgage prepayments, and debt repayment should be evaluated with your timeline, rates, and cash-flow needs in view.

- Starting small, choosing the right registered account, and investing consistently can matter more than waiting for perfect conditions.

Ready to run your numbers?

Use calculators and guides to test the assumptions that apply to your own finances.

What's on this page

Eight common Canadian personal finance rules deserve a closer look. This guide explains how to think about renting, TFSAs, raises and tax brackets, mortgage prepayments, starting to invest, debt, RRSPs, and market timing.

Eight Canadian personal finance misconceptions that deserve a closer look

Personal finance advice often arrives in the form of a tidy rule. Buy a home as soon as possible. Max out an RRSP before you think about a TFSA. Clear every dollar of debt before investing. Wait for the market to settle down before you put money to work. These ideas sound responsible because each one contains a small piece of truth. The trouble starts when a useful consideration hardens into a universal rule.

Canadian finances rarely reward one-size-fits-all thinking. Housing decisions depend on location and time horizon. Registered accounts behave differently. Tax brackets are progressive. A good debt plan should distinguish a credit-card balance from a low-rate mortgage. Investing becomes more approachable when you stop waiting for a perfect starting point.

This guide walks through eight common misconceptions and explains the more useful question behind each one. The aim is not to hand you a new collection of rigid rules. It is to make the next decision easier to reason through.

1. Renting is throwing away money

Rent pays for housing. You receive a place to live, flexibility, and freedom from many ownership costs. That does not make renting a guaranteed bargain, and it does not make homeownership a guaranteed investment win. The useful comparison is the full cost of each option over the period you expect to stay.

A homeowner may build equity as the mortgage principal falls, but ownership also includes interest, property taxes, insurance, maintenance, repairs, transaction costs, and the opportunity cost of the down payment. A renter may face rent increases and less control over the property, while keeping more flexibility and potentially investing money that would otherwise sit in a down payment or cover ownership costs.

The Financial Consumer Agency of Canada's renter guide recommends building a budget that includes rent, utilities, tenant insurance, deposits, and moving costs. That same full-cost mindset belongs in any rent-versus-buy decision.

- Buying can make sense when you expect to stay long enough for the transaction costs and ownership responsibilities to fit your life.

- Renting can make sense when flexibility matters, upfront costs are a constraint, or ownership costs are high relative to rent.

- Run the comparison with your own city, down payment, mortgage rate, rent, and timeline.

Go deeper with Canooq's rent-versus-buy calculator and should I buy a home in Canada guide.

Run your rent-versus-buy numbers

Compare renting and investing with buying a home using your own timeline, down payment, mortgage rate, and expected costs.

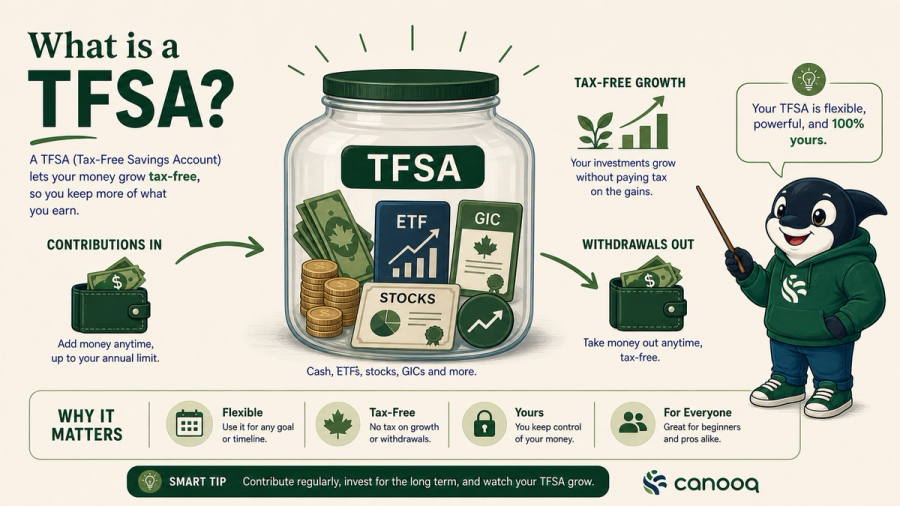

Open calculator2. A TFSA is just a savings account

The name causes a surprising amount of confusion. A Tax-Free Savings Account can hold savings, but it is not limited to a bank savings account. Think of the TFSA as a tax shelter with contribution rules. The investment or savings product inside the account does the actual work.

The CRA TFSA guide explains that a TFSA can hold qualified investments such as cash, mutual funds, listed securities, GICs, bonds, and certain shares. Contributions are not tax deductible, while investment income and withdrawals are generally tax free.

The right holding depends on your goal. Emergency savings may belong in a TFSA savings account when contribution room is available and easy access matters. A long-term retirement goal may use a diversified investment portfolio inside the TFSA. A short-term home repair fund usually should not be exposed to stock-market swings.

- Choose the goal first: emergency fund, short-term purchase, or long-term investing.

- Choose the investment second: cash, GICs, or a diversified investment portfolio.

- Track your contributions and withdrawals so you do not accidentally overcontribute.

Useful TFSA links

Use these before contributing or choosing investments inside a TFSA.

3. Getting a raise can leave you with less money after tax

Canada uses progressive tax brackets. When part of your taxable income moves into a higher bracket, the higher rate applies to the dollars inside that bracket. It does not reach backward and apply to every dollar you earned earlier in the year.

The CRA's federal income-tax rate page puts it plainly: individuals pay different tax rates on different portions of their taxable income. Provincial or territorial income tax follows its own brackets and rates.

Your take-home pay can change for several reasons after a raise, including payroll deductions, pension contributions, benefits, and income-tested programs. Those details deserve attention. The tax-bracket misconception is still worth clearing up because fear of earning more can lead people to turn down opportunities based on faulty math.

A simple way to think about it: your marginal tax rate applies to your next dollar of taxable income, while your average tax rate reflects the tax paid across your income as a whole.

Check the raise math

Use salary and tax tools before making decisions based on tax-bracket fear.

4. Paying off your mortgage is always the best move

Mortgage prepayments can be a strong financial move. Reducing principal gives you a guaranteed return equal to the mortgage interest you avoid, within the limits and rules of your mortgage contract. The word always is where the advice becomes less useful.

Extra cash may have several jobs competing for attention: building an emergency fund, clearing high-interest debt, contributing to a workplace retirement plan with an employer match, saving for a near-term expense, investing for long-term goals, or paying down the mortgage. The best order depends on your rates, cash-flow stability, available account room, comfort with investment risk, and timeline.

A household with no emergency reserve and a credit-card balance probably has a more urgent use for spare cash than an additional mortgage payment. A household with stable savings, no expensive debt, and a strong preference for a lower mortgage balance may reasonably prioritize prepayments.

- Check your mortgage prepayment privileges before sending extra money.

- Compare the guaranteed interest savings with your other priorities.

- Keep enough accessible savings for repairs, job changes, and ordinary surprises.

Mortgage tradeoff tools

Compare mortgage pressure with the rest of your household plan.

5. Investing is only worthwhile if you have a lot of money

A large starting balance can accelerate progress, but it is not the price of admission. Investing is often built from ordinary contributions repeated over a long period. A monthly amount that fits your budget can teach you how your account works, make the habit automatic, and give compounding time to do some of the heavy lifting.

The Ontario Securities Commission's investing-over-time guide encourages regular investing and explains that trying to predict short-term market movements can mean missing some of the market's strongest days.

Starting small does not mean investing carelessly. Your emergency savings, expensive debt, time horizon, diversification, fees, and risk tolerance still matter. A small contribution to a diversified investment can be a sensible beginning when the rest of your financial foundation is ready.

- Choose an amount you can repeat without creating cash-flow stress.

- Automate the contribution after payday.

- Review fees and diversification before chasing recent performance.

Start small, model the habit

A modest contribution becomes easier to judge when you can see the long-term math.

6. You need to be debt-free before you start investing

Debt changes the investing decision because interest is a guaranteed cost. High-interest consumer debt deserves serious attention, and clearing it can be one of the most effective uses of available cash. The broader claim that every dollar of debt must disappear before any investing begins can miss important details.

FCAC's debt-management guidance recommends listing what you owe, understanding the interest rates, making payments on time, and choosing a repayment strategy. That inventory helps you distinguish an urgent balance from a manageable one.

Someone carrying a high-rate credit-card balance will usually have a compelling reason to focus there first. Someone with a manageable student loan or mortgage, an adequate emergency fund, and access to an employer retirement match may reasonably combine debt repayment with long-term investing.

- Protect minimum payments and avoid missed-payment fees.

- Prioritize high-interest debt aggressively.

- Consider whether delaying all investing would mean giving up an employer match or valuable years of compounding.

- Keep the plan simple enough to maintain through an ordinary month.

Debt and investing next steps

Use these to separate urgent debt from manageable debt.

7. RRSPs are always better than TFSAs

The RRSP and TFSA are both useful registered accounts, and neither one wins every comparison. The RRSP can give you a tax deduction for eligible contributions. Withdrawals are generally taxable. TFSA contributions do not create a tax deduction, while withdrawals are generally tax free and the withdrawn amount is added back to contribution room in the following calendar year.

The Ontario Securities Commission's RRSP-versus-TFSA comparison highlights the practical differences. RRSPs are designed around retirement savings and tax deferral. TFSAs offer more flexible tax-free withdrawals and can serve short-term or long-term goals.

Your income now, expected income later, employer plans, contribution room, goal, and need for flexibility all matter. A worker in a high tax bracket may value an RRSP deduction. Someone building an emergency reserve or saving for a medium-term goal may prefer TFSA flexibility. Many households use a TFSA and RRSP together rather than forcing every savings dollar into one account.

- RRSP: consider the value of the deduction today and the tax treatment of withdrawals later.

- TFSA: consider the flexibility of tax-free withdrawals and restored contribution room in the next calendar year.

- FHSA: if you qualify and are saving for a first home, compare its specific benefits too.

Compare registered accounts

Use account-specific tools before assuming the RRSP always wins.

8. You should time the market and invest at the right moment

Waiting for the perfect moment feels cautious. In practice, it asks you to make two difficult calls: when to stay out and when to get back in. Markets do not send a clear signal when uncertainty has passed. By the time the news feels comfortable, prices may already have moved.

The Ontario Securities Commission's investing-over-time guide explains that missing some of the market's best days can affect long-term performance and that short-term movements are difficult to predict.

A regular contribution plan can reduce the pressure to make one dramatic decision. This approach does not guarantee a profit and it does not remove market risk. It gives long-term investors a process that can survive an ordinary news cycle.

- Use money that fits your time horizon and risk tolerance.

- Diversify rather than betting your plan on one investment or one prediction.

- Automate contributions when a regular plan fits your finances.

- Review your plan on a schedule instead of reacting to every headline.

Build the plan instead of timing the market

Use these to focus on contribution habits and account choice.

What these misconceptions have in common

Each misconception takes one reasonable idea and stretches it too far. Homeownership can build equity. Mortgage prepayments can reduce interest. Debt can limit your options. RRSP deductions can be valuable. Markets can fall after you invest. None of those truths becomes a universal instruction on its own.

The same principle applies when current events affect your finances. A Bank of Canada rate announcement can be a useful prompt to review mortgage and debt numbers, but it should not turn into a rushed decision without your own cash-flow and timeline in view.

Better decisions usually come from a short list of inputs: the interest rate, tax treatment, available account room, time horizon, goal, emergency fund, monthly cash flow, and your willingness to accept uncertainty. Once those inputs are visible, the loudest rule on social media becomes much easier to evaluate.

Frequently asked questions

Is renting always cheaper than buying?

No single answer works across Canada. Compare rent with the full cost of owning in your city and over your expected timeline. Include interest, taxes, insurance, maintenance, transaction costs, and the opportunity cost of the down payment.

Can I invest inside a TFSA?

Yes. A TFSA can hold qualified investments, including cash, GICs, bonds, mutual funds, and listed securities. Choose holdings that fit your goal and time horizon.

Can a higher tax bracket reduce my take-home pay from a raise?

A higher bracket applies to the portion of taxable income inside that bracket. Payroll deductions and income-tested benefits can change as income rises, so review the full picture, but a higher bracket does not retroactively tax every dollar at the new rate.

Should I pay off debt or invest first?

Start by listing the debt, interest rates, minimum payments, and emergency savings. High-interest debt often deserves priority. Lower-interest debt may sometimes be managed alongside long-term investing, especially when an employer match or a long time horizon matters.

Should I use an RRSP or TFSA first?

It depends on your income, goals, flexibility needs, contribution room, and expected tax situation. Many Canadians use both accounts for different purposes.

Bottom line

Personal finance becomes easier when you replace universal rules with better questions. What does this choice cost? What tax treatment applies? How soon will I need the money? Which risks am I taking? What happens if life gets expensive for a few months?

The goal is not to optimize every dollar perfectly. A good financial setup should be understandable, flexible, and sturdy enough to keep working while your life changes.

Related articles:

Page details

Author: Canooq Editorial

Updated: June 1, 2026

Cite this page: Canooq.ca, 8 Canadian Personal Finance Misconceptions That Can Lead You Astray, https://canooq.ca/blog/canadian-personal-finance-misconceptions

Canooq content is educational and may include affiliate or referral links. It is not financial, tax, legal, immigration, employment, mortgage, real estate, or healthcare advice. Verify official sources and provider terms before acting.